In 1997, a single financial move by billionaire investor George Soros set off a chain reaction that shook the entire Asian continent. By shorting the Thai Baht, Soros not only exposed the fragility of emerging markets but also pushed countries like Thailand, Indonesia, Malaysia, and South Korea into severe economic turmoil.

To many in Asia, this was not just a story of market correction — it was an economic assault that left millions jobless, currencies devalued, and entire systems restructured under the weight of IMF-driven reforms.

As India watched from the sidelines, the message was clear: global finance could bend even sovereign economies.

The Spark: Thailand’s Currency Collapse

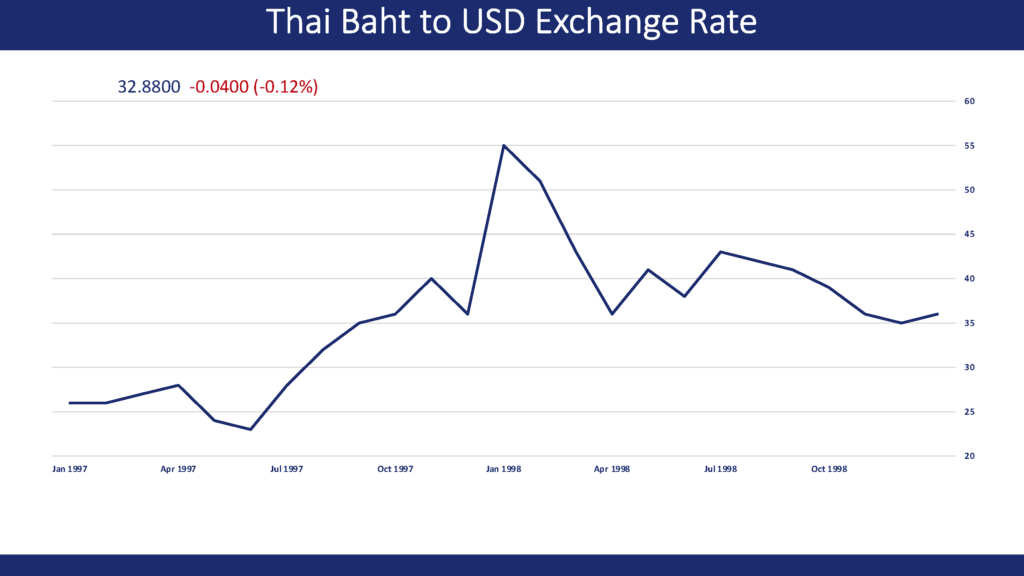

The crisis began in July 1997, when Soros’s Quantum Fund bet heavily against the Thai Baht. For years, Thailand had maintained a fixed exchange rate against the US dollar. However, excessive foreign borrowing and property speculation had made its economy fragile.

When speculators like Soros began selling Baht in massive quantities, the central bank’s reserves ran dry. Forced to float the currency, Thailand saw its Baht lose more than 50% of its value within months.

This single event triggered a domino effect across East Asia. Investors fled from neighbouring economies fearing similar weaknesses — and soon Indonesia, Malaysia, and South Korea found themselves in freefall.

Interview Insight: A Witness from the Frontline

To understand the crisis from within, Take The Lede spoke to Professor Dr. Marie-Aimée Tourres, a French development economist based in Malaysia and author of “The Tragedy That Didn’t Happen.”

Professor Tourres recalls:

“The fall of the Baht was not just economic contagion; it was psychological. Overnight, faith in Asian stability disappeared. Even countries with strong fundamentals suffered from investor panic.”

Her perspective matters because she lived through the meltdown while teaching in Kuala Lumpur. She watched the Malaysian Ringgit devalue sharply, businesses shut down, and public confidence erode almost overnight.

Key Impact of the 1997 Asian Financial Crisis

| Country | Currency Depreciation (1997–98) | GDP Contraction | IMF Bailout (USD) |

| Thailand | 56% | –10.5% | $17.2 billion |

| Indonesia | 80% | –13.1% | $43 billion |

| South Korea | 47% | –6.9% | $58 billion |

| Malaysia | 45% | –7.4% | Refused IMF aid |

Why Soros Targeted the Baht

The logic behind Soros’s move was simple yet ruthless. He had already earned fame (and infamy) for “breaking the Bank of England” in 1992 by shorting the British pound. In Thailand, he saw a similar weakness — overvalued currency, heavy debt, and weak fiscal control.

By borrowing Baht and selling it for dollars, Soros bet that Thailand would be unable to defend its peg. When that prediction came true, he re-bought Baht at a lower rate, profiting massively.

Professor Tourres points out:

“The markets operate without conscience. But when speculation becomes large enough to distort entire economies, it becomes a moral question.”

The Domino Effect: From Bangkok to Jakarta

Once Thailand’s economy crumbled, global investors began pulling capital from across Southeast Asia. The Indonesian Rupiah fell nearly 80%, and thousands of firms went bankrupt.

In Malaysia, Prime Minister Mahathir Mohamad accused Soros of waging “financial warfare” against developing nations. He imposed capital controls and pegged the Ringgit to the dollar — a move that Western economists criticised but later credited for stabilising Malaysia’s recovery.

Meanwhile, South Korea accepted an IMF bailout worth $58 billion, one of the largest in history, leading to mass layoffs and corporate restructurings.

Human Cost: Asia’s “Invisible Recession”

Behind the graphs and numbers was a human tragedy. Millions of workers lost their jobs as companies collapsed under foreign debt. The urban poor in Jakarta, Kuala Lumpur, and Bangkok bore the brunt of food inflation and unemployment.

In Indonesia, riots erupted in 1998, toppling President Suharto after 32 years in power. In Malaysia, small traders and factory workers faced a decade-long struggle to rebuild.

Professor Tourres summarises it best:

“The 1997 crisis was not just about economics — it reshaped how Asian societies viewed globalisation itself.”

India’s Lesson: Shielding the Rupee

India, though less exposed to global capital at the time, learned crucial lessons. The Reserve Bank of India (RBI) strengthened foreign exchange reserves, regulated short-term debt, and later introduced a market-determined exchange rate to prevent speculative attacks.

In a 2004 policy paper, then-RBI Governor Y.V. Reddy warned:

“Financial openness without institutional depth is like opening your gates during a storm.”

That cautious approach helped India avoid the worst effects of subsequent crises, including the 2008 global crash.

Rethinking Soros: Villain or Visionary?

To some, Soros remains a symbol of ruthless capitalism, a man who profits from chaos. To others, he is a visionary investor who merely exposes the inefficiencies of fragile economies.

Professor Tourres, however, takes a nuanced view:

“Soros didn’t cause the crisis alone. The foundations were already weak — corruption, crony capitalism, and speculative bubbles. But his actions accelerated the inevitable.”

This distinction matters because it reframes Soros not as a destroyer, but as a catalyst for systemic reform — however painful it may have been.

Malaysia’s Recovery and Political Fallout

When Malaysia rejected IMF aid, it became an exception in the region. Prime Minister Mahathir Mohamad’s decision to defy Western financial orthodoxy initially drew sharp criticism from global economists. But over time, his capital control measures and the decision to fix the Ringgit at 3.80 per USD proved stabilising.

Within two years, Malaysia’s growth rate recovered, inflation eased, and the banking system stabilised. However, this success came at a political cost. Mahathir’s deputy, Anwar Ibrahim, who advocated IMF-style reforms, was removed from office and later imprisoned, deepening domestic political rifts.

The crisis, thus, did not just reshape financial structures — it altered political alignments and the balance between economic liberalisation and national sovereignty.

Indonesia: Collapse, Reform, and a New Order

If Malaysia’s response was defiant, Indonesia’s experience was catastrophic. The Rupiah’s collapse from 2,400 to over 16,000 against the dollar destroyed public confidence. With inflation soaring and fuel prices doubling, riots broke out in Jakarta and Surabaya.

By May 1998, President Suharto, in power since 1967, was forced to resign. His downfall marked not only the end of an era but also the beginning of democratic reform in Indonesia.

Under the IMF’s supervision, Indonesia implemented wide-ranging reforms: cutting subsidies, dismantling monopolies, and privatising state-owned firms. Yet the social cost was immense — unemployment exceeded 15%, and poverty rates doubled in just one year.

The crisis laid bare how speculative attacks and internal corruption could together destroy an economy from within.

South Korea’s Debt-for-Democracy Moment

In South Korea, the financial crisis created both despair and unity. Citizens queued up to donate personal gold to help pay off the nation’s foreign debt. The gesture became symbolic of national resilience.

While the IMF bailout imposed austerity and labour reforms, it also paved the way for corporate transparency and a more democratic financial system. By 2001, South Korea had repaid its entire IMF loan ahead of schedule — a rare success story amid Asia’s wreckage.

However, the restructuring came at a price. Many chaebols (family-owned conglomerates) were broken up or forced into mergers, and unemployment surged among middle-class workers.

Soros’s Defence and the Debate on Ethics

George Soros has repeatedly rejected accusations that he “broke Asia.” In multiple interviews, he claimed his actions simply revealed weaknesses that governments ignored for years.

In his words:

“Markets can’t be blamed for exposing economic mismanagement. Speculators profit when systems are unsound.”

Critics, however, argue that large-scale currency speculation isn’t neutral. When hedge funds move billions overnight, they can create self-fulfilling crises, eroding trust and destabilising national economies.

The debate continues: should global finance be regulated like trade and defence, or is it simply an extension of free-market logic?

Comparing Asia’s Crisis to 2008 Global Meltdown

The 1997 crisis became a blueprint for understanding contagion — how fear spreads faster than facts. It exposed how dependent emerging markets were on short-term capital flows and foreign debt.

A decade later, the 2008 global financial crisis echoed similar themes — speculative leverage, overexposure, and regulatory failure — only this time, the epicentre was Wall Street.

Professor Tourres notes:

“The 1997 Asian crisis was the rehearsal. The 2008 collapse was the global performance.”

For India and other developing economies, the lesson was to build stronger reserves, diversify exports, and control hot money inflows.

Lessons for India and the Global South

India escaped the 1997 disaster largely because of its limited exposure to speculative capital. But the warning signs remain relevant today as the rupee faces periodic volatility and foreign portfolio flows rise sharply.

To prevent similar contagion, experts recommend:

- Maintaining large foreign exchange reserves.

- Strengthening financial regulation and monitoring external debt.

- Curbing short-term speculative inflows.

- Encouraging long-term investment over portfolio speculation.

These measures, while technical, protect nations from becoming collateral damage in the games of global finance.

The Broader Legacy of 1997

More than two decades later, the 1997 Asian financial crisis remains a defining moment for the Global South. It shifted the political mindset from blind liberalisation to strategic caution.

In hindsight, Soros’s gamble exposed not only Asia’s vulnerabilities but also the moral limits of speculative capitalism. It forced nations to ask whether economic growth can be left entirely to market forces or if sovereignty requires a degree of financial protectionism.

The crisis also shaped the rise of regional cooperation mechanisms like ASEAN+3 and the Chiang Mai Initiative, designed to provide mutual financial support during future shocks.